Crypto and the 2021 Rise of NFTs

At the end of 2021, an estimated 300 million individuals worldwide owned some form of cryptocurrency. The two greatest forces behind crypto adoption have been DeFi and NFTs.

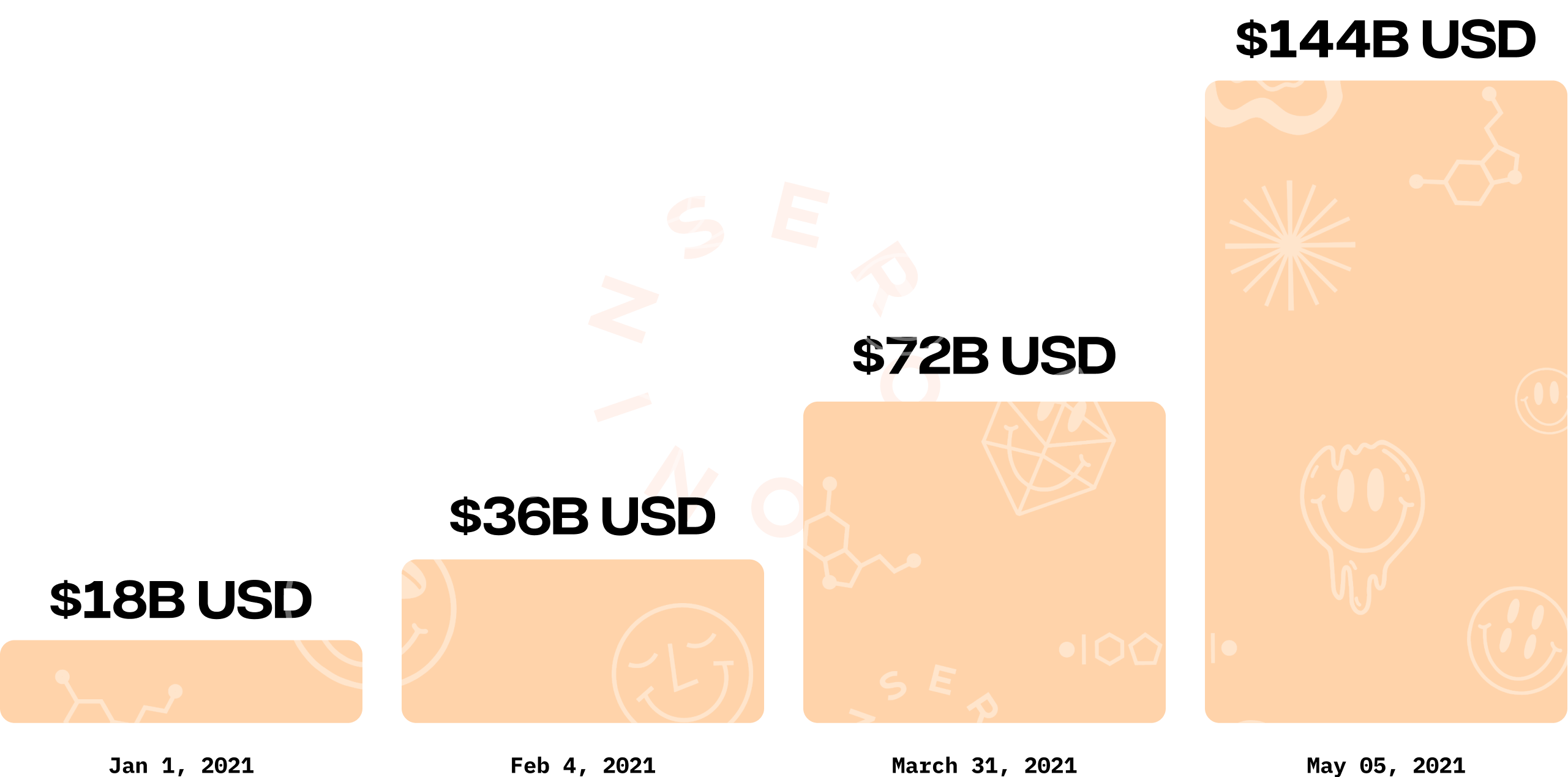

DeFi TVL Grows 40,000% in 24 Months

In 2020, “DeFi Summer” spurred an $18b USD increase in total value locked (TVL) across networks. In the first 5 months of 2021, DeFi TVL doubled three times, reaching $144b USD by May 5, 2021. The average time in between each doubling was less than 6 weeks.

In one year, DeFi TVL underwent a +1,200% increase (Jan. 1 - Dec. 31, 2021). This was following 2020’s unprecedented +3,340% increase in TVL. In total, the DeFi market TVL experienced a 40,000% increase in just 24 months. This is at a time period when just 16% of Americans have adopted cryptocurrency. Contextually, in 1996 only 16% of Americans had adopted the internet.

DeFi continues to attract significant consumer demand, but it has not undergone widespread adoption by large institutions and household brands. Only NFTs have unlocked the capacity of major brands to monetize their digital IP in a compliant, user-friendly, brand-preserving, and brand-building way.

NFT Trading Volume Grows 280,000% in 24 Months

In the second half of 2020, the crypto community began seeing an uptick in NFT activity, led largely by CryptoPunk sales.

Cumulative ETH spent on CryptoPunks QoQ, 2020.

Source: Dune Analytics.

Beginning in 2021, NFT sales accelerated as major drops garnered more attention and veteran players began entering the field. Projects of particular note in the first few months of 2021 included ArtBlocks x Hideki Tsukamoto Singularity (January), Christie’s x Beeple record-breaking $69M Everydays (March), the “rescue” of the 2017 project MoonCats (March), Sotheby’s x Pak The Fungible (April), and Yuga Labs x Allseeingseneca BAYC (April).

The result was parabolic growth in the trading volume on leading NFT platforms, dominated by Opensea on the Ethereum network. In December 2021, leading on-chain Ethereum NFT marketplaces did just under $5B USD in trading volume. A year prior, in December 2020, the monthly volume stood at $11.2M (a +44,000% increase).

Contrast NFT and DeFi numbers with the total value of the world’s capital markets and the impact of both past growth, and future potential comes into clear focus. According to the IMF, crypto assets accounted for nearly 5% of the U.S stock market capitalization in September 2021. But even with massive movement in DeFi and NFT adoption over the past year, these numbers pale in comparison to the global equities market cap, estimated by SIFMA to be around $120 trillion in early 2022. This leaves inordinate upside opportunity for continued growth in both categories.

Brands and the Rise of web2.5

Web2.5 is the adoption of web3 assets like NFTs within web2 infrastructure that allows for strong discovery, user experience, and brand retention.

As NFTs attracted breakneck retail spending in early 2021, large brands began taking note. Unlike DeFi, which presented opaque regulatory and compliance risk for major brands, NFTs provide an opportunity to retain digital IP and activate online communities in ways that were never before possible.

However, we have not yet seen a “web3-native” approach towards NFTs from any major brand. By that, we mean that no brand has upended their web2 architecture and replaced it entirely with a web3 stack. Instead, brands have taken a more measured approach, exploring NFT drops, integrations, and community growth developed separately from their core offerings. In short, brands have realized that web3 isn’t an ultimatum. They can explore emerging technologies like NFTs to both their benefit and that of their consumers without requiring immediate, all-in adoption.

What these brands have transitioned into is a model we call web2.5. They have combined the best of web3 (novel technologies, digital IP, and technical composability), with the proven web2 models of development, growth, and promotion. Fundamentally, that’s what web2.5 is: the adoption of web3 assets like NFTs within web2 infrastructure that allows for strong discovery, user experience, and brand retention.

In web2.5, brands use web3 technology, partnerships, and techniques to break through the noise, but typically sandbox this experimentation away from their core product lines.

Web2.5 isn’t particularly new. Some of the most popular and highly-valued blockchain companies (Coinbase, Gemini, Nifty Gateway) have adopted a web2.5 approach to crypto. They all rely on elements of web2 centralization to accelerate growth, ensure compliance, and enable UX — and therefore are not technically web3-native in its purest form. Notably, these companies have contributed to some of the greatest popular knowledge and adoption of cryptocurrency globally. Far from being a limiting compromise, the web2.5 model has proven one of the most powerful platforms for crypto and NFT visibility and adoption.

The blockchain community ended 2021 with an ecosystem of traditional companies that found their own ways to adopt web3. All of these efforts, no matter how large, small, or (un)successful, operated within the boundaries of web2.5. The macro story these brands tell is that we have a clear, steady, and high-opportunity path ahead of us towards web3.

Web2.5 is a waypoint on the spectrum, not the ultimate destination.